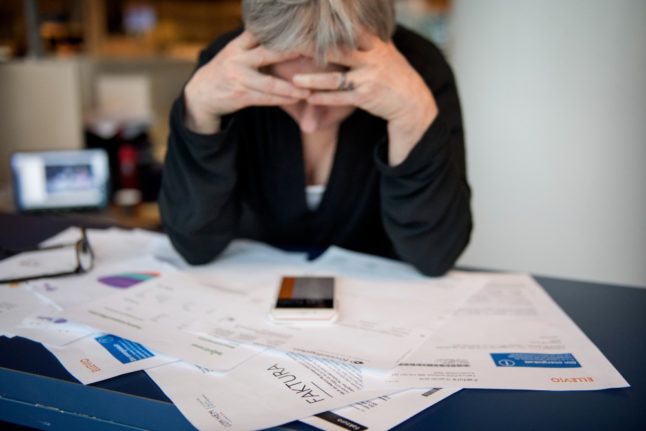

Households that were on the margins of being able to make ends meet are increasingly likely to be unable to pay bills.

The situation is reflected by an increasing number of outstanding bills referred to debt collection agencies in late 2022, news wire TT writes.

“Unfortunately, this is the consequence of the very large increases in costs for households,” Fredrik Engström, lawyer and chairperson of industry organisation Svensk inkasso (Swedish Debt Collection) told TT.

“Those who were already on the margin before are now having a very difficult time and many have suffered with payment difficulties,” he said.

Electricity bills in winter months can be some of the most difficult to pay for households, and inflation and high gas prices in late 2022 have made the cost of heating and electricity higher than usual.

READ ALSO:

- Sweden had its highest inflation in over 30 years in November

- What to do if you can’t pay your electricity bill in Sweden

Debt collection company Intrum now receives between 10 and 15 percent more debt collection cases for energy and electricity bills compared to a year earlier, TT writes.

Engström said that no dramatic increase in energy bill debts in particular had been seen during the autumn, however.

This may be due to those bills being prioritised over others, he added.

“You don’t want to risk the heat being turned off,” he said.

“There is a natural order of priority which households that have difficulty paying bills tend to follow. Rent, electricity and telephone bills usually come first,” he said.

Other late payments that might be referred to collection agencies can include both large and small loans as well as rolling costs like gym membership, broadband or other subscription fees.

Although Intrum has noted an increase in debt collection cases, Swedish consumers so far have shown a relatively good ability to withstand the cost of living crisis when it comes to paying bills according to Morten Trasti, chief analyst at Intrum Scandinavia.

This may be due to unemployment in Sweden remaining relatively low and many households having had the opportunity to save during the Covid-19 pandemic.

“If you compare the general case inflow today with how it looked during the same period before the pandemic, the number of debt collection cases has also decreased by approximately 7 percent” Trasti said.

The numbers are similar to those from March 2020 and the trend is comparable in Norway and Denmark, he added.

In September last year, Svensk inkasso asked its approximately 40 members if they had seen an increase in referrals in line with rising prices. Half of the companies said they had seen an increase of around 10 percent.

Engström said he would not be surprised to see a similar increase at the beginning of 2023.

“If the situation on the labour market gets worse, more Swedish households could have payment problems,” Trasti said.

“That is key for how the situation develops in future: how much unemployment rises,” he said.

Member comments