Non-resident foreign buyers only snapped up 1 percent of French properties that were sold last year, figures that have dropped almost threefold over the last ten years.

A fresh French property market report from Les Notaires has found that the proportion of non-resident foreign buyers has fallen sharply in France.

After a peak of 2.8 percent in 2006-2007, the figure dropped to 1.4 percent in 2014 and then down to 1 percent last year.

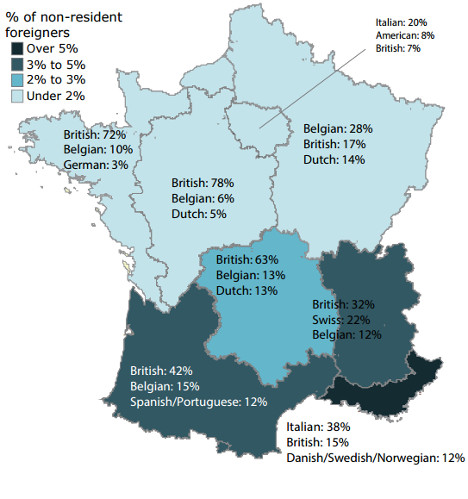

The report noted that foreign buyers were most represented by those from the UK – by far. In fact, British buyers made up 32.6 percent of the total non-resident buyers in France last year.

They were especially house-hungry in central and western France, as shown in the map below. In these areas British buyers made up between 70 and 80 percent of foreign buyers.

The next most common nationality was Italian, at 15.3 percent, followed by Belgium at 11.1 percent.

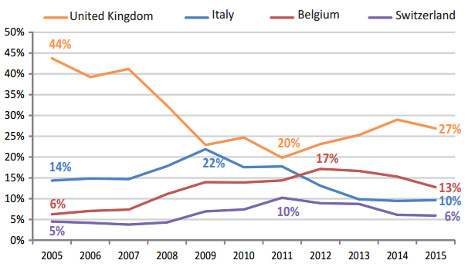

Les Notaires noted the percentage of British buyers has dropped massively over the last ten years.

In the graph below, the percentage of buyers from the UK dropped 17 points from 44 percent in 2005 to 27 percent in 2015. The graph only measures the four biggest buyers – those from the UK, Italy, Belgium, and Switzerland.

Despite this, the Brits have still outnumbered other nationalities the whole time.

Elsewhere in France, the only region where the national averages differ notably is in the Greater Paris region of Ile-de-France, where the main nationalities represented are both different and more diversified than in other regions.

When it came to foreigners, homes in Paris last year were most popular with Italians (at 20 percent), followed by Americans and Brits (at 8 and 7 percent respectively). Next it was Algerians (6 percent) and Moroccans (4 percent).

Despite the survey's figures the financial climate for foreigners, or at least Brits, to buy a house in France remains positive.

A combination of a strong pound and a drop in house prices in parts of France means that there are some real bargains out there for property hunters.

“All the stars and planets are aligned to give customers a good base to buy from,” Heather Byrne, Regional Manager at estate agents Leggett Immobilier for the Rhône-Alps told The Local recently.

She says that home prices are at their lowest since the 2008 crisis and that it's the best exchange rate in recent memory.

According to Leggett, the average UK buyer of French Alpine property spends around £290,000 – this time last year that would have bought you €342,000, but today it would fetch €390,000.

But it's not just about the favourable exchange rate.

“On top of that, French mortgage rates are also at an all-time low. It's the same as in the UK, the government wants the markets to be opened up and for people to keep selling to generate movement across the economy,” Byrne told The Local.

Member comments